Tracking Trends in Wireless Infrastructure

This file type includes high resolution graphics and schematics when applicable.

Wireless communications has evolved through four generations of technology to its current state: a hybrid vehicle for voice, video, and data using handheld and stationary electronic devices. It is the infrastructure—the towers, antennas, and associated hardware and software—that make all this possible, and it is the infrastructure that has driven a good part of the commercial RF/microwave market for the past 20 years. Although it is impossible to see the future, some of the technology advances that lead to the Fourth Generation (4G) of wireless communications may provide some insight into what will be needed for the next generation of wireless infrastructure equipment, and some of the technology evolution to come.

Wireless technology has been embraced worldwide as it continues to expand in a growing number of applications, both indoors and outdoors. Wireless communications customers continue to demand increased services in terms of voice, video, and data communications. These growing demands are driving cellular/wireless carriers and service providers to expand their wireless infrastructure to achieve higher data rates and increased capacity to serve the increased requirements of a growing customer base.

“Wireless infrastructure” is a term generally associated with the equipment and buildings needed to make cellular communications possible (Fig. 1), beginning with the erection of towers, antennas, and associated electronic equipment with the expansion of analog first-generation (1G) cellular communications systems in the 1980s. Successive generations of cellular equipment employed digital technology and modulation formats, with 3.5G cellular infrastructure currently the most dominant technology in use. However, fourth-generation (4G) cellular formats—such as WiMAX and Long Term Evolution (LTE) cellular technologies—are rapidly gaining ground.

1. Large towers with their cellular antennas are an ever-present reminder of the infrastructure needed to support wireless communications networks. [Photo courtesy of Huber + Suhner.]

Although the transmission/reception technologies change, the need for towers and the associated infrastructure still exists. Typically, the infrastructure represents a considerable investment in a cellular network, and existing towers will support multiple generations of cellular technologies; service providers will try to make the most efficient use of (possibly) 2G, 3G, and 4G equipment, all on the same tower.

Some general trends that are driving the expansion of wireless infrastructure include the growing number of mobile wireless communications users and the increasing amount of data being communicated via mobile networks. Cellular customers are even starting to use near-field-communications (NFC) technology to make on-site bill payments, adding to the amount of data on a cellular network. For their part, cellular service providers must find ways to accommodate the growing demands for data and bandwidth, while at the same time manage their own infrastructure operating expenses. The latter consist of capital equipment expenses (CAPEX), such as the cost of the cellular towers and wireless transceiver equipment, and operating expenses (OPEX), such as the electricity needed to run the cellular towers.

In some cases, increased wireless coverage can be increased through the use of smaller cell sites, known as femtocells, which can be installed in buildings and within public gathering places (e.g., shopping centers). They must also adopt “green” strategies for their wireless networks, since many service providers are managing heterogeneous networks consisting of a variety of different technologies (such as 2G, 3G, and 4G) together. A major OPEX is the electrical power needed to maintain the wireless network. Any green strategies that can save operating power can also result in significant savings in OPEX. In addition, improvements in spectrum efficiency, the use of advanced antenna techniques, such as multiple-input, multiple-output (MIMO) antenna configurations, and the use of smaller cells to expand coverage can all contribute to lower OPEX.

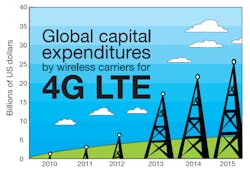

Clearly, LTE technology has captured the fancy of wireless service providers and will be the wireless standard of choice for expanding infrastructure in the next few years. According to a recent report by market research firm IHS iSuppli Wireless Communications, LTE will capture the majority of wireless infrastructure capital spending over the next several years as mobile service providers and carriers seek to provide their customers with the combination of coverage and services that is often difficult to support with earlier generations of cellular technology. According to the IHS iSuppli market study (Fig. 2), global capital spending on LTE technology is projected to reach $24.3 billion (USD) in 2013, or almost triple the level of spending on LTE technology in 2012.

2. Market studies project strong growth in the use of LTE technology in wireless base stations in the next several years. [Plot courtesy of IHS iSuppli Wireless Communications.]

The expected size and growth rate of 4G LTE technology has spurred its share of market research and positive expectations, including a study by Reportlinker, “The Wireless Infrastructure Market 2012-2017: Wi-Fi, WiMAX, 3G, HSPA+ and LTE,” which examines the projected market shares for a number of different technologies vying to support cellular communications. This report sets the value of the global wireless infrastructure market at $43 billion (USD) by the end of 2012. The report also makes some important points about how network operators must assess both their CAPEX and OPEX when installing and maintaining wireless infrastructure. The backhaul connections could be a limiting factor in terms of the number of subscribers that can be served by a specific infrastructure configuration. Put simply, when a cellular subscriber connects to a cellular antenna tower, the backhaul equipment connects them to the rest of the world.

Among the firms that are contributing to that expanding wireless infrastructure is the Swiss company Huber + Suhner, perhaps best known for its wide range of connectivity solutions. Sprint, one of the largest telecommunications companies in the US, is upgrading its 4G LTE towers to Huber + Suhner’s fiber-to-the-antenna (FTTA) for added bandwidth in its wireless infrastructure equipment, including in the backhaul portion of its networks. Huber + Suhner is now the leading supplier for 4G LTE installation systems in North America, helping to upgrade equipment for numerous large telecommunications companies [including Sprint, T-Mobile, Bell Mobility, SaskTel, and Telus (in Canada)], all with more than 10 million subscribers. According to a Huber + Suhner report, Sprint plans to upgrade around 15,000 cell sites within the next three years, while T-Mobile alone will upgrade more than 14,000 antenna masts in the US over the next 12 months. With the FTTA connectivity, the cellular transceiver electronics can be mounted near the antennas (on the mast), rather than as remote radio heads (RRHs) in cabinets on the ground, helping to speed and simplify installations.

Increasingly, carriers are viewing the maintenance and operation of their cellular infrastructure as an additional business, on top of serving their wireless communications subscribers. This has created opportunities for third-party companies to serve as wireless tower/equipment installers and maintainers, providing turnkey wireless infrastructure solutions for cellular/wireless carriers. As an example, Multiband Corp. offers an extensive list of wireless-infrastructure-related capabilities, including communications site construction with both RF/microwave and digital design and installation, site surveys, inspections, repair and maintenance, and even necessary preparation for Federal-Communications-Commission (FCC) site licensing. These third-party companies run the wireless infrastructure as a business, thereby freeing cellular carriers to focus on their primary responsibilities.

Large cell sites are beginning to share wireless communications traffic, with much smaller sites in the years to come—many within buildings, malls, and other public gathering places. In a market study by Maravedis-Rethink, “Transforming the Mobile Data Network: Operator Strategies for Profitable Small Cell Networks 2012-216,” which is based on a global survey of mobile wireless communications operators, two-thirds of smaller cellular base stations will be operating in bands above 2.2 GHz by 2016. This projects to several years of strong growth for smaller cell sites from 2013, when the number of small sites in bands above 2.2 GHz is less than 40%.

Both 3G and 4G equipment will be used in the smaller cells, in spectrum of 2.3 GHz and above. According to the report, the deployment of public-access small cells for 3G/4G services will rise from less than 30,000 in 2011 to about 11.3 million by 2016, or CAPEX investment of about $4 billion. The smaller cells enable additional mobile communications capacity in the short-distance areas that they cover, such as in and around shopping malls, which will generate new revenue streams for the carriers. Of course, securing locations for these smaller cells, managing the cells, and making effective backhaul connections will add to the complexity of adding smaller cells to existing cellular network infrastructure.

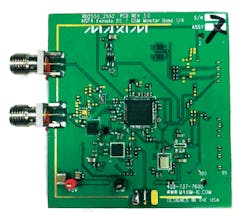

In support of smaller cell sites, a number of companies have developed integrated-circuit (IC) or system-on-chip (SoC) solutions that essentially incorporate most of the radio components and many of the digital components needed for a complete cellular base station. For example, the MAX2550 transceiver IC from Maxim Integrated Circuits can be supplied as part of a package with a reference design (Fig. 3) and operating software for installing a cellular femtocell. The package includes additional power amplifiers, duplexers, a temperature-controlled crystal oscillator (TCXO), software drivers, and all necessary passive circuit elements. The package even includes a performance report on how the radio design complies with the Third-Generation-Partnership-Program (3GPP) TS25.104 home-area base-station standard. The transceiver IC and reference design operate over a base-transceiver-station (BTS) receive band of 1920 to 1980 MHz and BTS transmit band of 2110 to 2170 MHz. It also supports downlink monitoring of surrounding cells. In addition, the company offers radio transceivers and reference designs for additional cellular bands, including full wideband-code-division-multiple-access (WCDMA) and cdma2000® coverage.

3. This reference design can be supplied for a number of different WCDMA and cdma2000 frequency bands for quick development of a wireless base station. [Photo courtesy of Maxim Integrated Circuits.]

On the digital side, Texas Instruments offers its model TMS320TCI6616 SoC, which combines cellular physical-layer (PHY) technology with high-speed packet processing capability. It features multiple TMS320C66x digital-signal-processing (DSP) cores, combining for essentially 4.8 GHz of equivalent DSP signal-processing capability. The SoC, which includes generous on-chip memory, can perform up to 76 billion floating-point operations per second (76 GFLOPS). It is ideal for use in smaller base stations, and provides the digital processing power without need of additional external components, such as field-programmable gate arrays (FPGAs).

Recently, Broadcom announced a universal digital front end which essentially could serve any number of different wireless platforms and standards with a single-chip solution. The single-chip model BCM51030 is designed to adapt automatically to any signal combination, including CDMA, WCDMA, and LTE signals. Ideal for smaller cell sites, it boasts improved efficiency with external amplifiers by means of the company’s VersaLine{TM} digital predistortion technology. It can work with any power amplifier technology, including with silicon LDMOS, GaAs, and GaN amplifiers.

These few devices are just a sampling of the radio and digital solutions to come, with an eye for operating at lower power levels in support of smaller, “greener” cell sites. The number of large sites with towers will be expanding, but that growth will be unmatched by the increase in smaller, mainly in-building wireless base stations.

This file type includes high resolution graphics and schematics when applicable.

About the Author

Jack Browne

Technical Contributor

Jack Browne, Technical Contributor, has worked in technical publishing for over 30 years. He managed the content and production of three technical journals while at the American Institute of Physics, including Medical Physics and the Journal of Vacuum Science & Technology. He has been a Publisher and Editor for Penton Media, started the firm’s Wireless Symposium & Exhibition trade show in 1993, and currently serves as Technical Contributor for that company's Microwaves & RF magazine. Browne, who holds a BS in Mathematics from City College of New York and BA degrees in English and Philosophy from Fordham University, is a member of the IEEE.